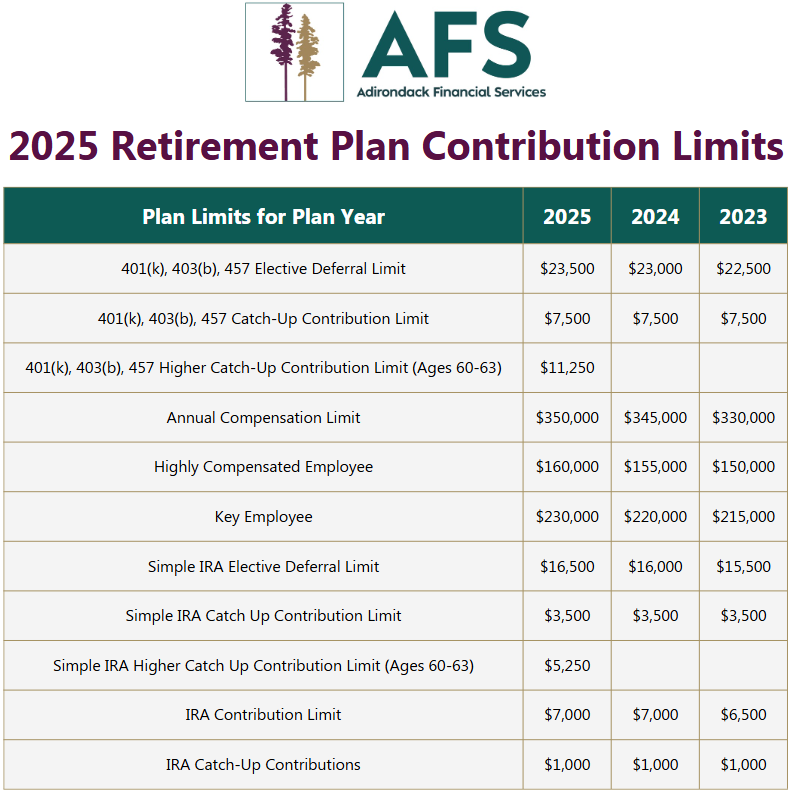

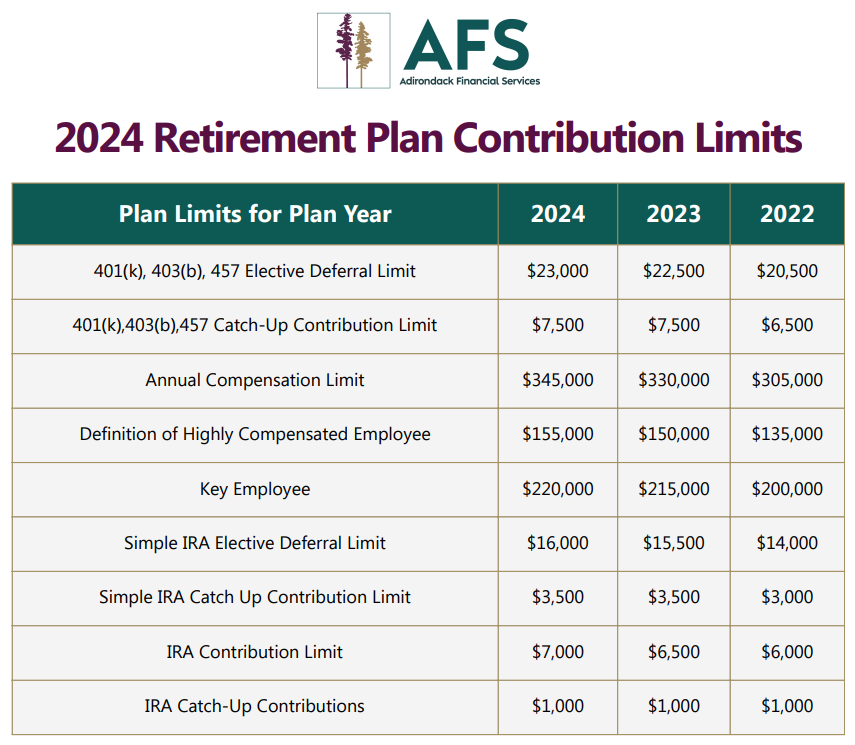

The IRS has officially announced the 2025 retirement plan contribution limits. Here are the highlights!

What Is Self-Funding?

Self-funding is one of the ways an employer can choose to offer a healthcare plan to their employees. An employer has a self-funded (or self-insured) group health plan if the employer assumes the financial risk associated with providing health care benefits to its employees. Instead of paying fixed premiums to an insurance company, the employer pays for medical claims out of pocket as they are incurred. Why would an employer choose self-funding? Check out the graphic below!

A Step-by-Step Scenario for How Self-Funded Benefits Work:

1. An employee makes an appointment with their doctor because they are sick.

2. The employee is then asked to provide their insurance card to their physician’s office personnel, which tells the doctor’s office what type of health plan they have, how it is administered and who the claim should be sent to.

3. A claim is generated and is submitted to the Plan Administrator.

4. The Plan Administrator will determine how the employee’s health benefits work and what payment is required for their doctor).

5. The Plan Administrator pays the provider based upon the plan benefits.

6. The Plan Administrator debits the employer’s bank account for the claim.

The Explanation of Benefits

After an employee’s visit with their physician, they will receive Explanation of Benefits, or EOB, from their health plan administrator. This EOB summarizes their claim, the payments they must make, the payments health plan must make, and any other payment information regarding their claim. This statement is not a bill or request for payment, it is simply informational.

What are an Employee’s Rights Under a Self-Funded Plan?

Self-funded health plans are regulated under the federal Employee Retirement

Income Security Act (ERISA), rather than state law

as insured health plans are. Federal regulations require an employer to provide

their employee with a summary description of their health plan and certain

other documents related to the plan. The employee can also request to see a copy

of the plan document that determines what benefits are available and how they

get paid.

Self-funded group health plans are also regulated by other applicable federal laws

including the:

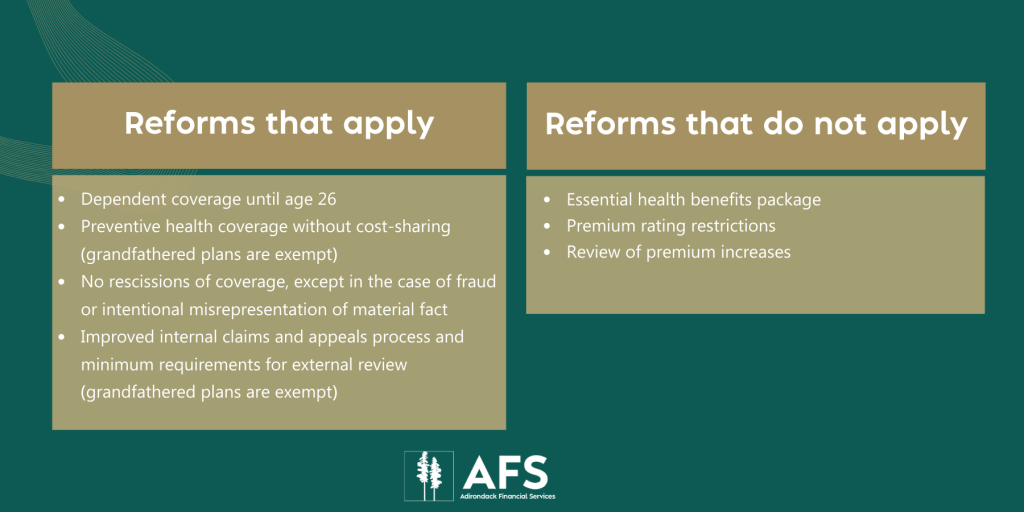

How has Health Care Reform made an impact?

Many health care reform regulations apply to all group health plans, regardless of

whether they are fully insured or self-insured, but self-insured plans are

exempt from certain provisions of health care reform. Check out the graphic

below to see examples of reforms that do and do not apply to self-insured

plans.

So, what can employees do?

Because the employer assumes the financial risk of providing an employee with health care benefits, the employer can either save or lose money depending on the level of claims incurred by their employees. Of course, employers want to be able to provide their employees with high quality health benefits, but as the cost of providing health care rises, employees too must do their part to keep benefits high and costs low.

What are some ways that employees can help save money for themselves and the company?

· Eliminate unnecessary visits to their doctor.

· Discuss healthy living and preventive care with their doctor.

· Follow prescription drug directions precisely.

· Be sure to take all their medication, even if they feel better.

· Use in-network providers if they have a Preferred Provider Organization (PPO) or Point-of-Service (POS) plan.

· Be a wise health care consumer and always ask questions if they do not understand the benefits available to them.

· Utilize Urgent Care facilities when appropriate, versus emergency rooms.

Adirondack Financial Services has expertise in transitioning organizations to self-funded health plans. Contact us for a free plan evaluation!

What is Medicare?

Medicare is health insurance for people who are age 65 or older, under 65 with certain disabilities or any age with end-stage renal disease (permanent kidney failure).

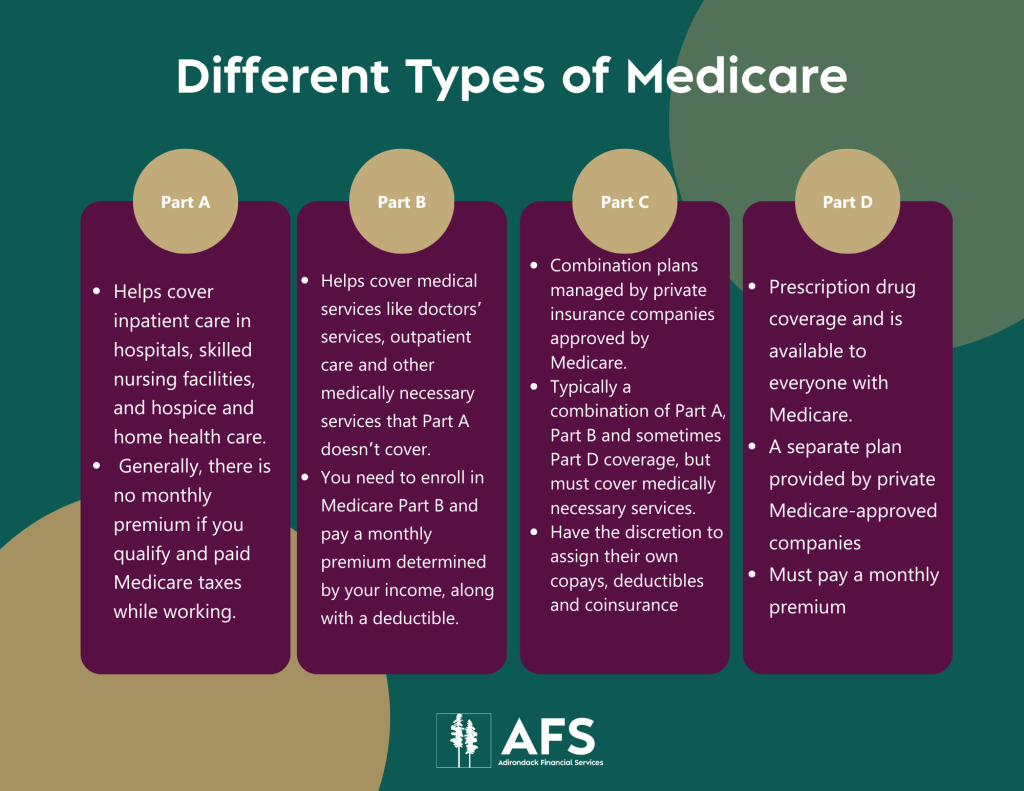

Types of Medicare

The are four different types of Medicare:

1. Medicare Part A

2. Medicare Part B

3. Medicare Advantage Plans (also known as Medicare Part C)

4. Medicare Part D

Many people also purchase a supplemental insurance policy, such as a Medigap plan, to handle any Part A and B coverage gaps. See Figure 1 for more information on the four types of Medicare!

A Step-by-Step Guide to getting started with Medicare:

1. Medicare will send you a questionnaire about three months before you’re entitled to Medicare coverage.

2. Your answers to these questions, including whether you have group health insurance through an employer or family member, help Medicare set up your file and make sure your claims are paid correctly.

3. Once you start Medicare, you should schedule a free preventive visit within the first 12 months to assess your current health status and create a health roadmap for the future.

If you have Medicare and another type of insurance, the question of who should pay or who should pay first can be tricky.

Contact a Licensed Adirondack Financial Services Medicare Specialist or call (315) 624-2617 (TTY: 711).

When times get tough, instinct often pushes people toward coping mechanisms. These mechanisms can help people feel like they’re escaping reality by relieving stress or distracting their minds. While this is a standard response, it can become problematic when one turns to harmful, unhealthy coping mechanisms. Common unhealthy coping mechanisms include oversleeping, excessive substance use, over- or under-eating and impulsive retail spending.

It’s expected to have feelings of wanting to escape from reality due to stress or anxiety. Healthy coping mechanisms can help you positively address such feelings and develop long lasting habits. Consider these healthier coping alternatives:

Unhealthy coping mechanisms can prevent you from reaching your short- and long-term goals. Making a task list of personal goals can help you achieve what you want and elevate your mood by physically seeing your accomplishments when they’re checked off the list.

Find someone willing to listen to you, such as a close friend, family member or mental health professional. Putting your feelings into words can help alleviate stress and anxiety.

Negativity is a normal part of Trying to avoid it is called avoidance behavior, which can result in reaching for unhealthy coping mechanisms.

Knowing what situations you negatively respond to can help you keep track of your triggers and be aware of how you react.

Activities such as painting or running can be therapeutic for many. Designate a regular time and space to practice your new hobby.

Having negative or overwhelming emotions is natural, but it’s important to lean on healthy coping mechanisms to help deal with stress and anxiety. Talk to your doctor or a mental health professional if you are experiencing ongoing emotional struggles.

© 2023 Zywave, Inc. All rights reserved.